Ten states have uninsured rates below 5 percent. What are they doing right?

Universal health care remains an unrealized dream for the United States. But in some parts of the country, the dream has drawn closer to a reality in the 13 years since the Affordable Care Act passed.

Overall, the number of uninsured Americans has fallen from 46.5 million in 2010, the year President Barack Obama signed his signature health care law, to about 26 million today. The US health system still has plenty of flaws — beyond the 8 percent of the population who are uninsured, far higher than in peer countries, many of the people who technically have health insurance still find it difficult to cover their share of their medical bills. Nevertheless, more people enjoy some financial protection against health care expenses than in any previous period in US history.

The country is inching toward universal coverage. If everybody who qualified for either the ACA’s financial assistance or its Medicaid expansion were successfully enrolled in the program, we would get closer still: More than half of the uninsured are technically eligible for government health care aid.

Particularly in the last few years, it has been the states, using the tools made available by them by the ACA, that have been chipping away most aggressively at the number of uninsured.

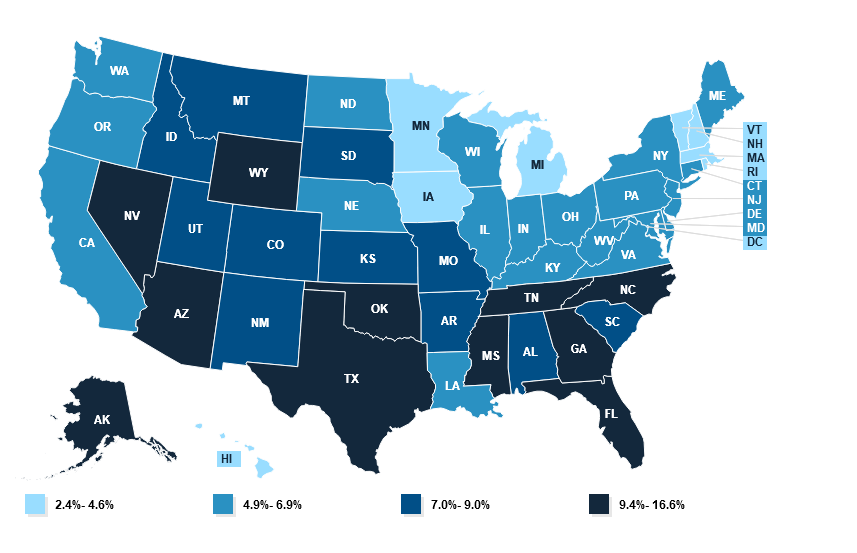

Today, 10 states have an uninsured rate below 5 percent — not quite universal coverage, but getting close. Other states may be hovering around the national average, but that still represents a dramatic improvement from the pre-ACA reality: In New Mexico, for instance, 23 percent of its population was uninsured in 2010; now just 8 percent is.

Their success indicates that, even without another major federal health care reform effort, it is possible to reduce the number of uninsured in the United States. If states are more aggressive about using all of the tools available to them under the ACA, the country could continue to bring down the number of uninsured people within its borders.

The law gave states discretion to build upon its basic structure. Many received approval from the federal government to create programs that lower premiums; some also offer state subsidies in addition to the federal assistance to reduce the cost of coverage, including for people who are not eligible for federal aid, such as undocumented immigrants. A few states are even offering new state-run health plans that will compete with private offerings.

I asked several leading health care experts which states stood out to them as having fully weaponized the ACA to reduce the number of uninsured. There was not a single answer.

“I don’t think any state has taken advantage of everything,” said Larry Levitt, executive vice president at the KFF health policy think tank. “No state has put all the pieces together to the full extent available under the ACA.”

But a few stood out for the steps they have taken over the last decade to strive toward universal health care.

Massachusetts (and New Mexico): Streamlined enrollment and state subsidies

Massachusetts has the lowest uninsured rate of any state: Just 2.4 percent of the population lacks coverage. It had a head start: The law provided the model for the ACA itself, with its system of government subsidies for private plans sold on a public marketplace that existed prior to 2010.

But experts say it still deserves credit for the steps it has taken since the Massachusetts model was applied to the rest of the country. Matt Fiedler, a senior fellow with the Brookings Schaeffer Initiative on Health Policy, said two policies stood above any others in expanding coverage: integrating the enrollment process for both Medicaid and ACA marketplace plans and offering state-based assistance on top of the law’s federal subsidies.

Massachusetts was among the first states to do both.

“The former can do a lot to reduce the risk that people lose their coverage when incomes change,” Fiedler told me, “while the latter directly improves affordability and thereby promotes take-up.”

Integrated enrollment means that, for the consumer, they can be directed to either the ACA’s marketplace (where they can use government subsidies to buy private coverage) or to the state Medicaid program through one portal. They enter their information and the state tells them which program they should enroll in. Without that integration, people might have to first apply to Medicaid and then, if they don’t qualify, separately seek out marketplace coverage. The more steps that a person must take to successfully enroll in a health plan, the more likely it is people will fall through the cracks.

The state assistance, meanwhile, both reduces premiums for people and makes it easier for them to afford more generous coverage, with lower out-of-pocket costs when they actually use medical services. Nine states including Massachusetts now have state assistance, with interest picking up in the past few years.

New Mexico, for example, only recently converted to a state-based ACA marketplace and started offering additional aid in 2023. Having already seen some dramatic improvements, it remains to be seen how much more progress the state can make toward universal coverage with that policy in place.

Minnesota and New York: The Basic Health Plan states

The basic structure of the ACA was this: Medicaid expansion for people living in or near poverty and marketplace plans for people with incomes above that. But the law included an option for states to more seamlessly integrate those two populations — and so far, the two states that have taken advantage of it, Minnesota and New York, are also among those states with the lowest uninsured rates. Just 4.3 percent of Minnesotans and 4.9 percent of New Yorkers lack coverage today.

They have both created Basic Health Plans, the product of one of the more obscure provisions of the health care law. This is a state-regulated health insurance plan meant to cover people up to 200 percent of the federal poverty level (about $29,000 for an individual or $50,000 for a family of three). Those are people who may not technically qualify for Medicaid under the ACA but who can still struggle to afford their monthly premiums and out-of-pocket obligations with a marketplace plan.

In both states, the Basic Health Plans offered insurance options with lower premiums and reduced cost-sharing responsibilities than the marketplace coverage that they would otherwise have been left with. In New York, for example, people between 100 percent and 150 percent of the federal poverty level pay no premiums at all, while people between 150 percent and 200 percent pay just $20 per month.

There is good evidence that the approach has increased coverage: In New York, for example, enrollment among people below 200 percent of the poverty level increased by 42 percent when the state adopted its BHP in 2016, compared to what it had been the year before when those people were relegated to conventional marketplace coverage.

State interest in Basic Health Plans has been limited so far, but Minnesota and New York provide a model others could follow. Fiedler said part of the basic plans’ success in those states has been using Medicaid managed-care companies to administer the plan: Those insurers already pay providers lower rates than marketplace plans do and the savings give the states money to reduce premiums and cost-sharing.

Colorado and Washington: Public options and assistance for the undocumented

These states have been inventive in myriad ways. They are both early adopters of a public option, a government health plan that competes with private plans on the marketplace, a policy also being tested in Nevada.

There is another policy that unites them, one that addresses a sizable part of the remaining uninsured nationwide: They both provide some state subsidies to undocumented immigrants.

Most uninsured Americans are already technically eligible for some kind of government assistance, whether Medicaid or marketplace subsidies. But there is a large chunk of people who are not: About 29 percent of the US’s uninsured are ineligible for government aid, among them the people who are in the country undocumented. Those people bear the full cost of their medical bills and may avoid care for that reason (among others, of course).

Starting this year, Washington is allowing undocumented people with incomes that would make them eligible for Medicaid expansion to enroll in that program, and making state subsidies available to people with higher incomes no matter their immigration status. Colorado has set aside a small pool of money annually to provide state aid to about 11,000 undocumented people. (After that threshold is hit, those folks can still enroll in a health plan but they must pay the full price.)

Interest has been robust: Last year, Colorado hit the enrollment limit after about a month. This year, enrollment capped out in just two days, suggesting the state may need to put more money behind the effort.

It is difficult to imagine insurance subsidies for undocumented people nationwide any time soon, given the fraught national politics of immigration. But states are finding ways to make inroads on their own: California has made undocumented people eligible for Medicaid.

Through these and other means, they are helping the US inch toward universal health care.

Dylan Scott covers health care for Vox. He has reported on health policy for more than 10 years, writing for Governing magazine, Talking Points Memo and STAT before joining Vox in 2017.